You’ve seen it on contractor websites, job listings, and business licenses: “bonded, licensed, and insured.” Most people nod along without knowing what “bonded” actually means — or why it matters. Here’s the short version: being bonded means a financial guarantee exists to protect someone else if you fail to meet your obligations. The moment that clicks, a lot of other things start to make sense.

Whether you’re a business owner trying to get bonded, a homeowner hiring a contractor, or a job seeker who just saw “must be bondable” on an application, this guide covers everything — what being bonded means, how it differs from insurance, who needs it, and what it actually costs.

The Core Meaning: What Does It Mean to Be Bonded?

Being bonded means a business or individual has obtained a surety bond — a legally binding, three-party agreement that financially guarantees an obligation will be met. If it isn’t, the party harmed can file a claim and receive compensation.

That three-party structure is what separates being bonded from every other type of financial protection. The three parties are always the same:

The Principal is the business or individual who obtains the bond and makes the promise to perform. The principal pays the bond premium and, critically, is responsible for reimbursing any claims the surety pays out.

The Obligee is the party who requires the bond — typically a government agency, licensing authority, project owner, or client. The obligee is protected if the principal fails.

The Surety is the bonding company — usually an insurance company with a surety department or a specialized bonding firm — that financially backs the principal’s promise. If a valid claim is filed, the surety pays the obligee and then seeks full reimbursement from the principal.

A real-world example: When the California DMV requires an auto dealer to obtain a surety bond before receiving a business license, the DMV is the obligee, the auto dealer is the principal, and the bonding company is the surety. If the dealer engages in fraudulent transactions, a harmed customer can file a claim against the bond.

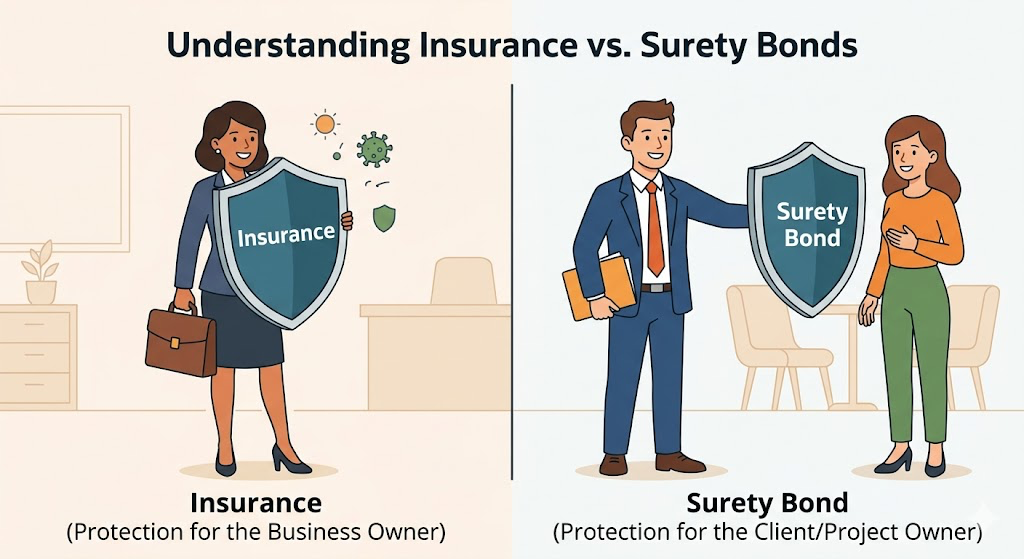

Being Bonded Is Not the Same as Being Insured

This is the single most misunderstood aspect of being bonded. Insurance and surety bonds both involve financial protection and both involve premiums — but they protect completely different parties, and claims are handled in completely opposite ways.

Insurance is a two-party agreement between the policyholder and the insurer. When a claim is filed, the insurer pays the policyholder. No repayment is required. Insurance protects you.

A surety bond is a three-party arrangement. When a claim is filed, the surety pays the obligee — not the principal. The principal then owes the surety the full amount paid, sometimes with interest and fees. A bond protects the other party, not you.

Think of it this way: a surety bond is less like insurance and more like a line of credit backed by a financial guarantee. The bonding company is effectively saying, “We’ve vetted this principal, and if they fall short, we’ll make it right — but they’ll pay us back.” That mechanism is what gives being bonded its credibility.

| Surety Bond | Insurance Policy | |

|---|---|---|

| Parties Involved | 3 — Principal, Obligee, Surety | 2 — Policyholder, Insurer |

| Who Is Protected | Clients / the public | The business itself |

| Claims Repayment | Principal must reimburse surety | No repayment required |

| Purpose | Guarantees performance and compliance | Covers unexpected losses |

| Loss Expectation | No losses expected | Risk of loss is assumed |

The Two Main Types of Bonds

Surety bonds and fidelity bonds are the two broad categories. Understanding the difference matters, because “being bonded” can mean either one depending on the context.

Surety bonds are the most common type for businesses and licensed professionals. They guarantee the principal will fulfill a legal or contractual obligation. They break into two major families: contract bonds (used primarily in construction — bid bonds, performance bonds, payment bonds, maintenance bonds) and commercial bonds (covering virtually everything else — license and permit bonds, court bonds, fiduciary bonds, freight broker bonds, auto dealer bonds, notary bonds, and more).

Fidelity bonds are different in purpose. Rather than guaranteeing a business’s performance to a client, fidelity bonds protect a business and its clients from dishonest acts by employees. A cleaning company that sends workers into people’s homes, a financial firm whose employees handle client accounts, or any organization with employees who have unsupervised access to money or property may carry fidelity bonds for exactly this reason. Fidelity bonds break into three subtypes:

Schedule fidelity bonds cover specific named employees. When someone leaves or joins, the list is updated and a background check is run on each listed individual.

Blanket position bonds cover entire job positions or roles rather than specific people — useful for businesses with high employee turnover.

Primary commercial blanket bonds cover all employees of a business regardless of rank or position, providing the broadest protection.

What Does “Bondable” Mean on a Job Application?

When an employer states “must be bondable,” they are not asking you to obtain a bond yourself — they are asking whether you are eligible to be covered by a fidelity bond the employer will take out on your behalf. Being bondable signals to the employer that you can pass the background check a bonding company will conduct. It is essentially a trustworthiness declaration.

Bondable jobs are most common in industries where employees have unsupervised access to money, property, or sensitive information: banking, finance, accounting, real estate, cleaning and janitorial services, home health care, plumbing, electrical work, and construction-related roles.

Factors that improve bondability include a clean criminal record, good credit history, an established work history, no substance abuse history, and an honorable military discharge for veterans. However, lacking some of these factors does not automatically disqualify a candidate. The U.S. Department of Labor runs the Federal Bonding Program specifically to help at-risk individuals — including ex-offenders, welfare recipients, those recovering from substance abuse, people with poor credit, and dishonorably discharged veterans — obtain employment by making them bondable at no cost to the employer.

Who Needs to Be Bonded?

A wide range of businesses and professionals either are required to be bonded by law or choose to be bonded to build credibility:

| Business Type | Bond Typically Required |

|---|---|

| Contractors and construction companies | License bond, performance bond, payment bond |

| Auto dealers | Motor vehicle dealer bond |

| Mortgage brokers and lenders | Mortgage broker bond |

| Freight brokers | BMC-84 FMCSA bond |

| Cleaning and janitorial services | Business services / fidelity bond |

| Travel agencies | Travel agency bond |

| Notaries public | Notary bond |

| Court-appointed guardians and executors | Probate / fiduciary bond |

| Medicare equipment suppliers | DMEPOS bond |

| Insurance brokers | Insurance broker bond |

Bonds are also required in some court proceedings, for employees managing pension and 401(k) plans (ERISA bonds), and for individuals needing to replace lost financial instruments or obtain vehicle titles when original documentation is missing.

The Benefits of Being Bonded

Being bonded does more than satisfy a legal requirement. For businesses, it signals financial vetting and professional accountability. Surety companies investigate applicants before issuing bonds — so the bond itself communicates to clients that an independent third party has reviewed the business and found it creditworthy. For clients and consumers, it provides a clear financial remedy if something goes wrong, without having to pursue costly litigation.

The practical benefits include the ability to operate legally in regulated industries, eligibility to bid on government and large private contracts that mandate bonding, enhanced consumer trust, and protection against the financial consequences of employee dishonesty or incomplete work.

How to Get a Bonded Business Bond

The process is more straightforward than most people expect. Apply by identifying the bond type and amount required by your obligee — a government agency, licensing board, or project owner will specify both. Submit your application to a licensed surety bond provider. Swiftbonds handles bonds across all types and all 50 states, making the process fast and accessible whether you need a simple license bond or a large construction bond. Once your application is reviewed and approved, you receive a Quote, Pay the premium, and File the bond with the obligee. Most license and permit bonds are approved the same day.

Swiftbonds LLC

2025 Surety Bond Agency of the Year

4901 W. 136th Street

Leawood KS 66224

(913) 214-8344

https://swiftbonds.com/

What Does Being Bonded Cost?

Bond premiums are typically calculated as a percentage of the total bond amount — generally between 1% and 15%. The exact rate depends on the type of bond, the required bond amount, and the principal’s credit history and financial strength. A contractor with excellent credit seeking a $50,000 license bond might pay as little as 1%–3% annually, while an applicant with poor credit on a high-risk bond may pay closer to 10%–15%.

Some smaller license and permit bonds carry flat annual premiums as low as $50 to $200. Larger construction bonds — performance and payment bonds on major projects — are priced more carefully because the risk is proportionally greater. Most bonds renew annually; some continuous bonds remain in effect until formally canceled by one of the parties.

FAQs About Being Bonded

What does it mean when a contractor says they are bonded? It means the contractor has obtained a surety bond, usually a license bond or contractor bond, that provides financial protection to clients if the contractor fails to fulfill obligations, engages in unethical behavior, or causes covered losses. It is a form of third-party accountability.

Is being bonded the same as having insurance? No. Insurance protects the business. A bond protects the client or obligee. If a bond claim is paid, the bonded business must reimburse the bonding company in full. No such repayment exists with standard insurance claims.

What does “bondable” mean on a job application? It means you are eligible to be covered by a fidelity bond your employer takes out on you. You would need to pass a background check by a bonding company. It signals trustworthiness — particularly relevant for jobs involving unsupervised access to money, property, or clients’ homes.

Can someone get bonded with bad credit? Yes, though the premium rate will be higher. Many bonding companies have programs for applicants with difficult credit histories. The Federal Bonding Program also provides no-cost fidelity bonds to help at-risk individuals secure employment.

Do you need to be bonded and insured? For most businesses, yes — because they serve different purposes. A bond protects your clients. Insurance protects your business. Both are often required simultaneously by government agencies, licensing boards, and project owners.

How long does a surety bond last? Most bonds are issued for one year and renewed annually. Construction bonds may expire when a project is complete. Continuous bonds have no fixed expiration and remain active until one party provides formal notice of cancellation, typically 30 to 60 days in advance.

What happens if a claim is filed against a bond? The surety investigates. If the claim is valid, the surety compensates the obligee up to the bond’s face value. The principal then owes the surety the full amount paid out, potentially plus interest and legal fees. Unpaid claims can also result in bond cancellation, which may jeopardize a business license or contract.

Conclusion

Being bonded is a verifiable commitment — a financial guarantee backed by a third party that gives clients, government agencies, and the public real recourse if something goes wrong. It differs fundamentally from insurance because it protects someone else, not the business that holds it. Whether you are a contractor building credibility, a job seeker proving trustworthiness, or a business owner meeting a legal requirement, understanding what it means to be bonded — and why it matters — puts you in a far stronger position in any regulated or trust-dependent industry.

5 Interesting Facts About Being Bonded Not Found in the Top 10 Sites

- The underwriting process for a surety bond is closer to a loan application than an insurance application. Surety companies review financial statements, credit scores, work history, and references before issuing a bond — because they expect to be repaid if a claim is filed. This is why getting bonded also serves as informal proof that your business finances are in order.

- Being bonded can actually lower your liability insurance premiums over time. Insurers view bonded businesses as lower risk because the vetting required for a bond signals stronger financial controls and more accountable business practices — making the business a more attractive insurance customer.

- In some industries, claiming to be bonded when you are not is a criminal offense. State contractor licensing boards in California, Texas, Florida, and others treat misrepresentation of bond status as fraud — subject to license revocation, fines, and in some cases criminal prosecution.

- Bond amounts are not arbitrary — they are often calculated based on potential harm. Government agencies typically set bond amounts equal to the maximum estimated financial damage that a bad-faith principal could cause consumers in their jurisdiction. A higher-risk license type almost always carries a higher required bond amount.

- A surety bond claim does not necessarily mean a payout happens. Sureties have the legal right to investigate and dispute claims — and in some cases, the surety may resolve the situation by requiring the principal to correct the problem directly rather than paying the obligee in cash. This mediation role is rarely mentioned but makes bonded disputes less adversarial than formal litigation.