You want to do business in Wisconsin. Whether you are an auto dealer, a mortgage broker, a money transmitter, or a check seller, one question comes up: do you need a surety bond? The answer is yes for many professions—and the amounts vary dramatically. A check seller needs a $10,000 bond. A mortgage broker needs $120,000. A money transmitter’s bond is set by the DFI based on volume. And auto dealers need bonds ranging from $5,000 to $50,000 depending on license type. This guide covers everything you need to know about Wisconsin surety bonds—the requirements, the costs, the statutes, and exactly how to get bonded.

What Is a Wisconsin Surety Bond?

A surety bond is a three-party agreement that guarantees a business will comply with state laws and fulfill its obligations to customers and the state. If the business fails to perform—through fraud, non-payment, code violations, or other misconduct—the bond provides financial compensation to the harmed party.

The three parties are:

- Principal: The business or individual who needs the bond

- Obligee: The Wisconsin state agency requiring the bond (e.g., Department of Financial Institutions, Department of Transportation)

- Surety: The company that issues the bond and backs the guarantee

If a claim is filed against the bond and found valid, the surety pays the claimant up to the bond amount. The business must then reimburse the surety in full.

Wisconsin Auto Dealer Bonds

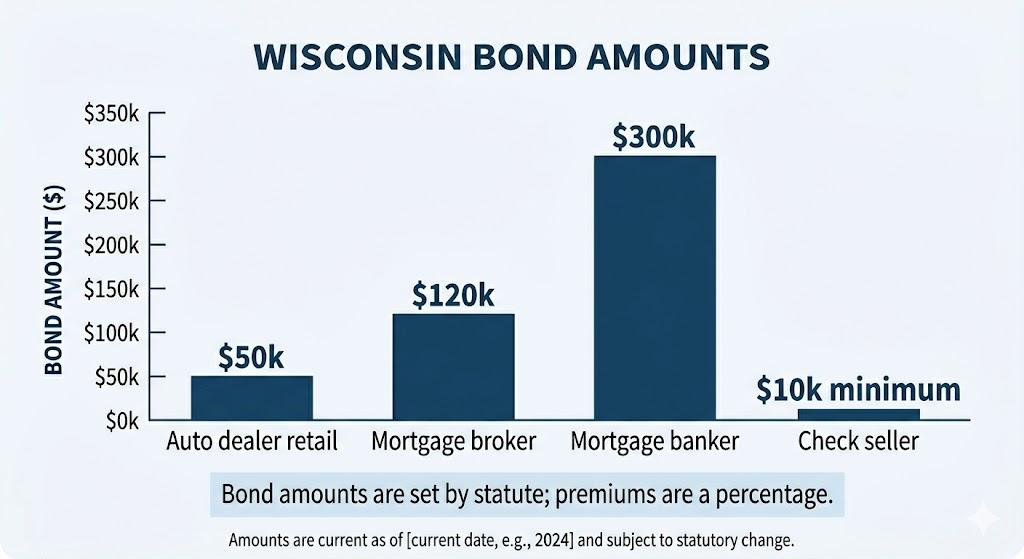

Every motor vehicle dealer in Wisconsin must obtain a surety bond as part of the licensing process with the Wisconsin Department of Transportation (DOT) . The bond protects consumers from financial harm caused by dealer misconduct, such as failure to deliver titles, unpaid taxes, odometer fraud, or other violations .

| License Type | Bond Amount | Starting Premium (Good Credit) |

|---|---|---|

| Retail dealer | $50,000 | $500/year |

| Wholesale, auction, salvage, RV dealer | $25,000 | $250/year |

| Motorcycle or moped dealer | $5,000 | $100/year |

Alternative security: Dealers may also submit an Irrevocable Letter of Credit (ILC) in lieu of a surety bond .

Premium rates: Underwriters review personal credit, business financials, time in operation, and overall stability. Dealers with strong credit histories often secure rates between 1% and 3% of the bond amount . Even if your credit is less than perfect, specialty programs can help you obtain the required coverage .

Wisconsin Mortgage Broker and Mortgage Banker Bonds

The Wisconsin Department of Financial Institutions (DFI) requires surety bonds for both mortgage brokers and mortgage bankers under Wisconsin Statutes Chapter 224 . These bonds provide assurance that a person impacted by a mortgage broker’s or banker’s unethical actions can be compensated fairly .

| License Type | Bond Amount | Typical Premium (Good Credit) |

|---|---|---|

| Mortgage broker | $120,000 | $1,200 – $3,600 |

| Mortgage banker | $300,000 | $3,000 – $9,000 |

Premium rates by credit score :

| Bond Amount | Credit 700+ | Credit 600-699 | Credit 599 or below |

|---|---|---|---|

| $120,000 | $1,200 – $3,600 | $3,600 – $6,000 | $6,000 – $12,000 |

| $300,000 | $3,000 – $9,000 | $9,000 – $15,000 | $15,000 – $30,000 |

Wisconsin Check Seller (Money Transmitter) Bonds

Under Wisconsin Statute 217.06(3)(a) , sellers of checks (money transmitters) must file a surety bond with the Division of Banking .

Bond amount: Minimum principal sum of $10,000 for the first location and an additional $5,000 for each additional location . The Division may determine that a bond in such amount is insufficient and may require a larger sum, but in no event shall the bond exceed $300,000 .

Purpose: The bond runs to the state for the benefit of any claimants against the applicant to secure the faithful performance of obligations with respect to the receipt, handling, transmission, and payment of money in connection with the sale of checks . It also reimburses the division for any examination or liquidation expense .

Important provisions:

- The aggregate liability of the surety in no event shall exceed the principal sum of the bond

- The surety has the right to cancel upon giving not less than 60 days’ written notice to the division

- Claimants may bring suit directly on the bond, or the attorney general may bring suit on behalf of such claimants

Alternative to bond: In lieu of a corporate surety bond, an applicant may deposit interest-bearing obligations of the United States, Wisconsin state, or local government securities with approved banks or trust companies .

Wisconsin Money Transmitter Bond

Under Wisconsin law, companies engaging in money transmission—including wire transfers, issuing payment instruments, or receiving money for transmission—must obtain a Money Transmitter Bond from the DFI .

Bond amount: The bond amount is determined by the volume of business and set by the DFI. The minimum bond amount is $10,000 and can increase based on transaction volume and risk profile .

Premium: The premium is calculated as a percentage (typically 1%–5%) of the total bond amount. For example, a $50,000 bond at a 2% premium rate would cost $1,000 annually . Businesses with strong credit and solid financial records often secure lower rates .

Wisconsin Financial Responsibility Bond (SR-22 Equivalent)

Under Wisconsin Statute 344.36, proof of financial responsibility may be evidenced by a bond of a surety company duly authorized to transact business within the state . The bond may also be a bond with at least two individual sureties each owning real estate within the state and together having equities equal in value to at least twice the amount of the bond .

- The bond shall be conditioned for the payment of amounts specified in s. 344.01(2)(d)

- The bond shall be filed with the secretary and shall not be cancelable except after 10 days’ written notice to the secretary

- The bond constitutes a lien in favor of the state upon any surety’s real estate scheduled in the bond

- If a judgment against the principal is not satisfied within 60 days after becoming final, the judgment creditor may bring an action in the name of the state against the surety

Important case law: The direct action statute, s. 632.24, does not apply to actions in which the principal on a bond under this section causes injury. Subsection (3) requires obtaining a judgment against the principal before an action may be brought against the surety (Vansguard v. Progressive Northern Insurance Co., 188 Wis. 2d 584).

Other Wisconsin Surety Bonds

Professional Fund-Raiser (Custodial) Bond

Wisconsin requires custodial bonds for professional fund-raisers. The bond protects the public by guaranteeing that the fund-raiser will follow state rules while operating . Even applicants with credit issues can obtain these bonds through specialty programs .

General Surety Provisions (Chapter 27)

Wisconsin statutes include general provisions for surety bonds, including that bonds need not be under seal (632.14) and validity of surety bonds (632.17) .

How Much Do Wisconsin Surety Bonds Cost?

The cost of a surety bond is the premium you pay to the surety company—a small percentage of the bond amount. Most applicants with good credit pay between 1% and 5% of the bond amount .

| Bond Type | Bond Amount | Starting Premium (Good Credit) |

|---|---|---|

| Auto dealer (retail) | $50,000 | $500/year |

| Auto dealer (wholesale/auction/salvage/RV) | $25,000 | $250/year |

| Auto dealer (motorcycle/moped) | $5,000 | $100/year |

| Mortgage broker | $120,000 | $1,200 – $3,600 |

| Mortgage banker | $300,000 | $3,000 – $9,000 |

| Check seller (first location) | $10,000 minimum | $100 – $300 |

| Money transmitter | Varies (min $10,000) | 1% – 5% of bond amount |

Factors affecting your premium:

- Personal credit score (primary factor)

- Business financial history

- Years in business and industry experience

- Bond amount required

How to Get a Wisconsin Surety Bond

The process follows four simple steps, and specialists like Swiftbonds have placed these bonds for Wisconsin businesses, working with A.M. Best A-rated sureties. Here is how it works:

- Apply: Complete a surety bond application with your business information, credit details, and the specific bond type and amount required by your Wisconsin agency.

- Quote: Within hours, the surety returns a premium quote based on your credit profile and the required bond amount.

- Pay: You pay the premium via credit card, ACH, or wire transfer.

- File: The surety issues the bond, and you file it with the relevant Wisconsin agency (DOT for auto dealers, DFI for mortgage brokers and money transmitters, etc.) as required.

Swiftbonds LLC

2025 Surety Bond Technology Provider of the Year

4901 W. 136th Street

Leawood KS 66224

(913) 214-8344

https://swiftbonds.com/

Cancellation Provisions for Wisconsin Bonds

Wisconsin law includes specific cancellation notice requirements for different bond types:

Alternative Security Options

Several Wisconsin statutes allow alternatives to surety bonds:

- Check sellers: May deposit interest-bearing obligations of the United States, Wisconsin state, or local government securities in lieu of a bond

- Auto dealers: May submit an Irrevocable Letter of Credit (ILC) instead of a surety bond

Frequently Asked Questions

Q: How much is an auto dealer bond in Wisconsin?

Retail dealers need a $50,000 bond (premium starts at $500/year). Wholesale, auction, salvage, and RV dealers need $25,000 (starts at $250/year). Motorcycle and moped dealers need $5,000 (starts at $100/year) .

Q: What is the bond amount for a Wisconsin mortgage broker?

Mortgage brokers must post a $120,000 bond. Mortgage bankers must post a $300,000 bond .

Q: Do check sellers need a bond in Wisconsin?

Yes. Under Wisconsin Statute 217.06(3)(a), check sellers must file a surety bond of at least $10,000 for the first location plus $5,000 for each additional location .

Q: Can I get a surety bond with bad credit in Wisconsin?

Yes. Many sureties offer programs for applicants with challenged credit, though premiums will be higher .

Q: What happens if a claim is filed against my bond?

The surety investigates. If valid, the surety pays the claimant up to the bond amount. You must then reimburse the surety in full .

Q: How long does a Wisconsin surety bond last?

Most license bonds are valid for one year and must be renewed annually. Some bonds are continuous and remain in effect until canceled.

Q: What is the cancellation notice period for a Wisconsin check seller bond?

The surety must give not less than 60 days’ written notice to the division before canceling .

Q: Where do I file my Wisconsin surety bond?

Auto dealer bonds are filed with the Wisconsin Department of Transportation. Mortgage broker and money transmitter bonds are filed with the Department of Financial Institutions. Check with your specific licensing agency.

5 Interesting Things About Wisconsin Surety Bonds Not in the Top 10 Sites

- Wisconsin allows individual sureties with real estate for financial responsibility bonds. Unlike most states that require corporate sureties, Wisconsin Statute 344.36 allows a bond with at least two individual sureties each owning real estate within the state with equities equal to at least twice the bond amount .

- The bond creates a lien on the surety’s real estate. Under Wisconsin law, the bond constitutes a lien in favor of the state upon any surety’s real estate scheduled in the bond. The lien is effective when the secretary records the bond in the county where the real estate is located .

- Check seller bonds have a $300,000 maximum. While the minimum is $10,000 for the first location, Wisconsin law caps the bond requirement at $300,000 no matter how many additional locations are added .

- Claimants can sue directly on check seller bonds. Under Wisconsin Statute 217.06(3)(a), claimants against the applicant may themselves bring suit directly on the bond, or the attorney general may bring suit on behalf of such claimants .

- Wisconsin mortgage bonds have different premium tiers based on credit.Unlike many states with flat rates, Wisconsin mortgage broker bonds have three distinct pricing tiers (excellent, average, and poor credit) ranging from $1,200 to $12,000 for brokers and $3,000 to $30,000 for bankers .

Conclusion

Wisconsin requires surety bonds for many professions, including auto dealers, mortgage brokers, check sellers, and money transmitters. Bond amounts vary significantly: retail auto dealers need $50,000 ; mortgage brokers need $120,000 ; check sellers need at least $10,000 for the first location ; and money transmitters need a minimum of $10,000 with amounts set by DFI based on volume .

The cost of a Wisconsin surety bond is a small percentage of the bond amount—typically 1-5% for applicants with good credit. A $50,000 auto dealer bond might cost $500 per year, while a $120,000 mortgage broker bond might cost $1,200-$3,600 per year .

Before applying for any Wisconsin surety bond, confirm the specific requirement with the relevant agency: the Department of Transportation for auto dealers, the Department of Financial Institutions for mortgage brokers and money transmitters, or the Division of Banking for check sellers. The bond is not optional for most licensed professions—it is a condition of doing business legally in Wisconsin.