Fuel distributors cannot legally operate in most states without posting a fuel tax bond first. These surety bonds guarantee that businesses selling, distributing, importing, or blending motor fuels will pay every dollar of state and federal fuel taxes owed. One missed tax payment triggers claims that can shut down operations, revoke licenses, and create devastating financial liability. State revenue departments mandate these bonds because fuel tax evasion costs governments billions annually while funding critical highway infrastructure and transportation programs.

Fuel tax bonds protect state governments from revenue losses while ensuring businesses comply with complex tax reporting requirements. Unlike insurance policies that protect the policyholder, surety bonds protect government agencies and taxpayers from fuel sellers who fail to remit collected taxes or violate licensing regulations.

What Is a Fuel Tax Bond

A fuel tax bond is a license surety bond required by state departments of revenue before fuel sellers, distributors, suppliers, importers, exporters, blenders, and dealers can obtain licenses to operate legally. The bond creates a binding three-party agreement between the fuel business purchasing the bond (principal), the surety company issuing the bond (surety), and the state agency requiring the bond (obligee).

This arrangement guarantees that fuel businesses will pay all required state fuel taxes, penalties, interest, and fees according to statutory deadlines and reporting requirements. The bond protects state revenue departments from tax losses when fuel businesses fail to remit collected taxes, file required reports, or comply with fuel licensing laws.

When fuel businesses violate tax requirements, state agencies can file claims against the bond to recover unpaid taxes up to the full bond amount. The surety company pays valid claims, then seeks full reimbursement from the fuel business. This reimbursement obligation distinguishes surety bonds from insurance and creates powerful financial incentives for tax compliance.

Most states require fuel tax bonds as mandatory licensing conditions. Operating fuel businesses without required bonds constitutes serious violations subject to license revocation, administrative penalties, and potential criminal prosecution depending on state statutes.

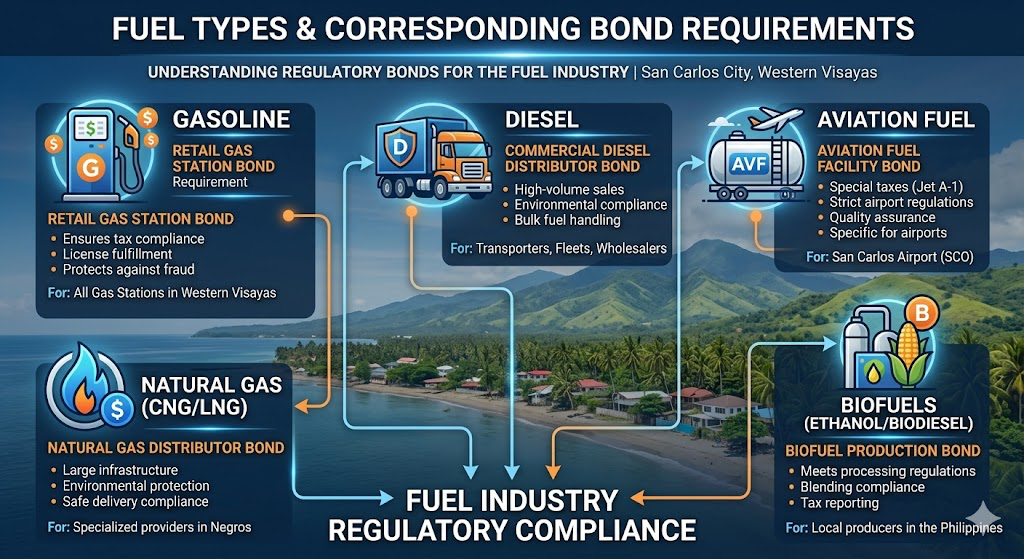

Types of Fuel Tax Bonds and Alternate Names

Fuel tax bonds appear under various names across different states and jurisdictions. Common designations include motor fuels tax bond, motor vehicle fuel tax bond, mileage and fuel tax bond, fuel distributor bond, fuel supplier bond, aviation fuel dealer bond, and International Fuel Tax Agreement bond. These variations reference the same fundamental bonding requirement with minor differences in specific coverage or business activities.

States often impose multiple fuel tax bond types based on business operations. Texas requires separate bonds for gasoline distributors, diesel fuel distributors, dyed diesel users, aviation fuel dealers, and compressed natural gas dealers. Each bond type carries distinct coverage amounts and premium rates based on specific fuel types and tax liabilities.

The International Fuel Tax Agreement bond covers interstate motor carriers traveling through multiple jurisdictions. IFTA streamlines fuel tax reporting by allowing carriers to report fuel consumption and taxes through one base jurisdiction instead of filing in every state traveled. The IFTA bond guarantees carriers will pay fuel taxes owed to all participating jurisdictions.

Federal operations require taxable fuel bonds filed with the Internal Revenue Service on Form 928. These federal bonds guarantee payment of excise taxes imposed on gasoline, diesel fuel, and kerosene under Internal Revenue Code sections 4041 and 4081. Federal bonds operate independently from state fuel tax bonds, and businesses often need both.

Who Needs a Fuel Tax Bond

Fuel tax bond requirements apply to businesses throughout the fuel distribution chain from importation through retail sale. Most states require bonds for fuel distributors, suppliers, wholesalers, importers, exporters, blenders, terminal operators, and retail sellers depending on business activities and licensing classifications.

Fuel distributors who receive fuel from suppliers or terminal operators for resale to retailers or end users typically need the highest bond amounts. These businesses handle massive fuel volumes and corresponding tax liabilities, creating substantial risk for state revenue departments.

Fuel suppliers and terminal operators who store and distribute fuel at wholesale levels face similar bonding requirements. Terminal operators maintaining storage facilities where fuel enters state tax systems often need additional bonding based on potential tax liabilities from all fuel passing through their terminals.

Blenders who mix fuels, dyes, or additives need specialized bonds covering tax obligations on blended products. Aviation fuel dealers supplying airports and aircraft operators require bonds ensuring payment of aviation fuel taxes. Compressed natural gas and liquefied natural gas dealers face growing bonding requirements as alternative fuels gain market share.

Retail fuel sellers generally face lower bonding thresholds than wholesale operations. Some states exempt small retailers from bonding requirements entirely while imposing bonds only on distributors and suppliers. Other states require universal bonding regardless of business size or fuel volume.

Multi-state fuel operators need separate bonds for each state where they conduct business. Bond coverage does not transfer across state lines, requiring businesses to navigate different requirements, amounts, and filing procedures in every jurisdiction.

Bond Amounts by State

Fuel tax bond amounts vary dramatically across states, ranging from one thousand dollars in Illinois to six hundred thousand dollars in Texas. Most states calculate required bond amounts using formulas based on estimated tax liabilities, fuel volumes, or business history.

| State | Bond Type | Minimum Amount | Maximum Amount | Calculation Method |

|---|---|---|---|---|

| Texas | Gasoline/Diesel | $30,000 | $600,000 | 2x maximum tax per reporting period |

| Texas | Dyed Diesel | $10,000 | $600,000 | 2x maximum tax per reporting period |

| Texas | CNG/LNG | $30,000 | $600,000 | 2x maximum tax per reporting period |

| Illinois | Financial Responsibility | $1,000 | Varies | Set by Department of Revenue |

| Georgia | Motor Fuel | $2,000 | $100,000 | Based on tax liability |

| Colorado | Fuel Distributor | $25,000 | $25,000 | Fixed amount |

| Oregon | Motor Fuel Dealer | Varies | Varies | Based on fuel volumes |

Texas uses the most aggressive bonding formula, requiring bonds equal to twice the maximum tax that could accrue during a reporting period. For gasoline and diesel distributors, this calculation produces bond amounts between thirty thousand and six hundred thousand dollars. Dyed diesel users face lower minimums at ten thousand dollars but the same six hundred thousand dollar maximum. Compressed natural gas and liquefied natural gas dealers must post bonds between thirty thousand and six hundred thousand dollars.

Illinois requires minimum one thousand dollar bonds set by the Department of Revenue based on individual business circumstances. Georgia mandates bonds between two thousand and one hundred thousand dollars depending on estimated tax liabilities. Colorado imposes fixed twenty-five thousand dollar bonds for all fuel distributors.

Federal taxable fuel bonds filed with the IRS follow different calculation methods. The Internal Revenue Service determines bond amounts ensuring timely tax collection based on applicant financial capabilities, tax history, and expected liability. Federal bonds cannot exceed the applicant’s expected tax liability for a representative six-month period plus terminal operator liability for one month.

Bond amounts often increase after businesses demonstrate higher fuel volumes or tax liabilities. States may require strengthening or superseding bonds when quarterly tax liabilities exceed amounts covered by existing bonds. Failure to increase bond coverage when required triggers immediate license suspension.

Fuel Tax Bond Costs

Fuel tax bond premiums typically range from one percent to ten percent of required bond amounts annually. The premium represents the cost paid to surety companies for guaranteeing bonds, not the total bond amount. Personal credit scores determine exact rates within this range for smaller bonds under fifty thousand dollars.

| Credit Score Range | Premium Rate | Cost for $25,000 Bond | Cost for $100,000 Bond |

|---|---|---|---|

| 700 and above | 1% – 3% | $250 – $750 | $1,000 – $3,000 |

| 650 – 699 | 3% – 5% | $750 – $1,250 | $3,000 – $5,000 |

| 600 – 649 | 5% – 7% | $1,250 – $1,750 | $5,000 – $7,000 |

| 550 – 599 | 7% – 10% | $1,750 – $2,500 | $7,000 – $10,000 |

| Below 550 | 10% – 15% | $2,500 – $3,750 | $10,000 – $15,000 |

Applicants with excellent credit scores above 700 pay premiums at the lowest end of pricing ranges, typically one to three percent of bond amounts. A fuel distributor with 750 credit score needing a twenty-five thousand dollar bond would pay approximately two hundred fifty to seven hundred fifty dollars annually. The same applicant requiring a one hundred thousand dollar bond would pay one thousand to three thousand dollars.

Applicants with poor credit below 600 face significantly higher premiums, often seven to fifteen percent of bond amounts. Someone with 550 credit score needing a twenty-five thousand dollar bond might pay one thousand seven hundred fifty to three thousand seven hundred fifty dollars. Higher bond amounts compound these costs proportionally.

Several factors beyond credit scores influence fuel tax bond pricing. Business financial statements become critical underwriting criteria for bonds exceeding fifty thousand dollars. Surety companies carefully evaluate business revenue, profit margins, liquid assets, debt ratios, and operating history before approving large bonds.

Prior tax compliance history affects pricing substantially. Businesses with clean tax records and no prior bond claims qualify for preferred rates even with moderate credit scores. Those with tax liens, payment defaults, or prior bond claims face higher rates or outright denials from standard markets.

Business structure impacts premiums as well. Corporations and limited liability companies typically receive better rates than sole proprietorships due to perceived financial stability and regulatory oversight. Established businesses with multi-year operating histories pay less than startups lacking proven track records.

Some high-risk applicants require collateral to secure bonds. Surety companies may demand cash deposits, letters of credit, or pledged assets for applicants with severe credit problems, substantial debt, weak financials, or prior claims history. Collateral requirements significantly increase total bonding costs beyond annual premiums.

Three-Party Structure and How Bonds Work

Every fuel tax bond involves three distinct parties with specific rights and obligations creating the surety relationship. The principal is the fuel business that purchases the bond and pays the premium. The obligee is the state agency requiring the bond, typically the Department of Revenue, Comptroller of Public Accounts, or similar tax authority. The surety is the insurance company that issues the bond and guarantees payment of valid claims.

When fuel businesses fail to pay taxes, file required reports, or comply with licensing regulations, state agencies file claims against bonds to recover losses. Common claim triggers include failure to remit collected fuel taxes by statutory deadlines, filing false or fraudulent tax returns, operating without valid licenses, selling fuel without proper tax stamps or dye markers, and violating fuel quality standards or environmental regulations.

The claims process begins when state agencies submit written claims to surety companies documenting tax deficiencies, regulatory violations, or unpaid penalties. Claims must include specific allegations with supporting evidence such as tax returns, payment records, audit findings, and regulatory violation notices.

Surety companies investigate each claim by requesting documentation from both the state agency and the fuel business. Investigation focuses on verifying tax amounts owed, confirming reporting deadlines missed, and determining whether violations occurred. Most fuel tax claims involve straightforward calculations comparing taxes collected versus taxes remitted.

When surety companies determine claims are valid, they pay state agencies up to the full bond penalty amount. The fuel business then owes the surety for the entire claim payment plus investigation costs, legal fees, and interest. This reimbursement obligation is absolute and enforceable through legal action regardless of the business’s financial condition.

Failure to repay surety companies results in immediate bond cancellation, license suspension, collection lawsuits, asset seizures, and potential bankruptcy proceedings. Surety companies aggressively pursue reimbursement because they guarantee bonds but assume no ultimate liability. The principal bears all financial responsibility for valid claims.

State-Specific Requirements

Different states impose unique fuel tax bond requirements based on local statutes, tax structures, and administrative procedures. Understanding these variations helps fuel businesses maintain compliance across multiple jurisdictions.

Texas requires the most comprehensive bonding system with separate bonds for gasoline distributors, diesel distributors, aviation fuel dealers, dyed diesel users, and natural gas dealers. The Texas Comptroller of Public Accounts calculates bond amounts as twice the maximum tax that could accrue during a reporting period. Bonds remain continuous without fixed expiration dates and renew automatically unless canceled with proper notice.

Illinois mandates Fuel Tax Financial Responsibility Bonds through the Department of Revenue for businesses using, selling, distributing, or mixing motor fuel. Illinois sets minimum bond amounts at one thousand dollars but increases requirements based on individual business circumstances and tax histories. The Illinois bond guarantees payment of all tax amounts becoming due under state law.

Georgia requires both Motor Fuel Tax Bonds and Motor Fuel Distributor Bonds ranging from two thousand to one hundred thousand dollars. Georgia bonds ensure compliance with Title 48, Chapter 9, Article 2 of Georgia law governing motor carrier operations and fuel taxation. Georgia bonds operate on continuous twelve-month terms with automatic renewal subject to premium payment.

Oregon requires separate bonds for motor fuel dealers, use fuel sellers, and use fuel users through the Oregon Department of Transportation Fuel Tax Group. Oregon bonds guarantee payment of all applicable taxes, fees, and penalties while ensuring compliance with Oregon Revised Statutes 319.010 through 319.880. Oregon imposes significant penalties for late filings and unpaid taxes, frequently resulting in bond claims.

Colorado mandates twenty-five thousand dollar Fuel Distributor Bonds through the Department of Revenue for one-year terms. Colorado bonds guarantee compliance with motor fuel and aviation fuel distribution regulations under Colorado Revised Statutes sections 39-27-101 through 39-27-218. Colorado requires prompt payment of all taxes, penalties, and interest due under state law.

Virginia offers two options for meeting fuel tax security requirements: surety bonds using Form FT462 or certificates of deposit with assignment forms. Virginia requires bonds from fuel suppliers, alternative fuel providers, and retailers who defer tax payments to providers. Bond amounts vary based on fuel volumes and business operations.

Federal requirements operate independently from state bonds. The Internal Revenue Service requires Taxable Fuel Bonds on Form 928 for businesses registered under section 4101 for gasoline, diesel fuel, or kerosene operations. Federal bonds ensure payment of excise taxes under Internal Revenue Code sections 4041 and 4081 with no fixed term or expiration date.

How to Get a Fuel Tax Bond

Getting a fuel tax bond requires four straightforward steps: application, quote, payment, and filing.

First, complete a surety bond application providing personal and business information. Applications require your name, social security number, business details, requested bond amount, and state jurisdiction. Most applications take ten to twenty minutes depending on bond complexity.

Second, receive your bond quote from the surety company. Underwriters evaluate your credit report and financial information to determine your premium rate. Applicants with good credit typically receive instant quotes for bonds under fifty thousand dollars. Those with credit challenges or requesting large bonds may need additional documentation but can still get approved through specialized programs.

Third, pay your premium. Surety companies accept credit cards, debit cards, electronic checks, and wire transfers. Payment processing takes minutes for electronic methods. Some companies offer premium financing for large bonds, allowing monthly payments instead of full annual premiums upfront.

Fourth, file your bond with the appropriate state agency. Your surety company provides original bond documents for submission to the Department of Revenue, Comptroller of Public Accounts, or designated licensing authority. Swiftbonds streamlines this entire process, offering same-day bond issuance for qualified applicants and expert guidance navigating state-specific requirements.

Swiftbonds LLC

2024 Surety Bond Provider of the Year

4901 W. 136th Street

Leawood KS 66224

(913) 214-8344

https://swiftbonds.com/

International Fuel Tax Agreement Requirements

The International Fuel Tax Agreement simplifies fuel tax reporting for interstate motor carriers operating in multiple jurisdictions. IFTA allows carriers to report fuel consumption and pay taxes through one base jurisdiction instead of obtaining licenses and filing returns in every state traveled.

IFTA member jurisdictions include all lower forty-eight states plus ten Canadian provinces. Carriers with qualified motor vehicles traveling through two or more member jurisdictions must register for IFTA licenses and credentials. Qualified motor vehicles include those with three or more axles, weighing over twenty-six thousand pounds, or used in combination exceeding twenty-six thousand pounds.

Many states require IFTA bonds guaranteeing carriers will pay fuel taxes owed to all participating jurisdictions. IFTA bond amounts vary by state based on estimated quarterly fuel consumption and tax liabilities. Some jurisdictions waive IFTA bonding requirements for carriers with excellent compliance histories or minimal fuel usage.

IFTA bonds protect revenue collection across all member jurisdictions. When carriers fail to file quarterly returns or pay taxes owed, any affected jurisdiction can pursue claims against the bond. This multi-state enforcement creates higher risk for surety companies, often resulting in stricter underwriting and higher premiums for IFTA bonds.

Carriers must maintain continuous IFTA bond coverage throughout license periods. Bond cancellations trigger immediate license suspensions across all IFTA jurisdictions, prohibiting interstate operations until coverage reinstates. Most carriers purchase annual bonds with automatic renewal to avoid gaps.

Operating Without Required Bonds

Operating fuel businesses without required bonds carries severe consequences. State agencies treat unbonded fuel operations as serious violations subject to criminal and civil penalties.

Administrative penalties include immediate license revocation prohibiting all fuel sales and distributions, cease and desist orders stopping business operations, monetary fines ranging from one thousand to fifty thousand dollars per violation, and permanent bars from future licensing. Each day of unbonded operation may constitute separate violations subject to individual penalties.

Criminal penalties vary by state but can include misdemeanor or felony charges depending on violation severity and tax amounts evaded. Convicted violators face fines, probation, and potential incarceration. Repeat offenders or those causing substantial tax losses may face enhanced penalties under state criminal statutes.

Tax collection actions represent another major risk. State revenue departments can seize business assets, garnish bank accounts, levy business income, and file tax liens against real property to collect unpaid fuel taxes. Without bond protection, businesses must satisfy these obligations from operating capital and personal assets.

Professional reputation damage from operating without bonds can permanently harm business prospects. Fuel suppliers and distributors verify licensing and bonding before establishing business relationships. Unbonded status signals unreliable operations and regulatory risk, making it nearly impossible to attract wholesale suppliers or retail customers.

Multi-state operators face compounding penalties when unbonded in multiple jurisdictions. Each state independently enforces bonding requirements, creating simultaneous penalties, license suspensions, and collection actions across all states where violations occurred.

Bond Renewal and Maintenance

Fuel tax bonds require annual renewal to maintain continuous coverage protecting business licenses. Surety companies typically contact bonded businesses thirty to sixty days before renewal dates to begin renewal processes.

Renewal procedures vary based on business performance and financial condition. Businesses with clean compliance histories and stable finances usually receive renewal quotes at similar rates to expiring policies. Those with tax payment issues, credit deterioration, or financial problems may face higher renewal rates or coverage denials.

Premium adjustments at renewal reflect changes in business risk profiles. Improved credit scores can reduce renewal rates by two to five percentage points. Tax liens, late payments, or compliance violations can increase rates by five to ten percentage points or trigger outright renewal denials.

Some businesses purchase multi-year bonds to lock in current rates and reduce administrative burden. Three-year bonds provide rate stability and eliminate annual renewal paperwork. However, they also prevent businesses from shopping for better rates if credit improves or market conditions change.

Timely renewal payment is critical because bond lapses trigger immediate license suspensions in most states. Fuel businesses cannot legally operate even one day without active bonds. Missing renewal deadlines requires reinstatement procedures that may delay business operations and incur additional fees.

Bond amount changes require new bonds or riders. When businesses expand operations increasing tax liabilities beyond current bond coverage, states require strengthening or superseding bonds. Strengthening bonds add coverage to existing bonds while superseding bonds completely replace them with higher amounts.

Frequently Asked Questions

What is a fuel tax bond?

A fuel tax bond is a license surety bond required by most states before fuel sellers, distributors, suppliers, importers, exporters, blenders, or dealers can obtain licenses to operate legally. The bond guarantees that fuel businesses will pay all required state fuel taxes, penalties, interest, and fees according to statutory requirements. If fuel businesses fail to remit collected taxes or comply with regulations, state agencies can file claims against bonds to recover losses.

Who needs a fuel tax bond?

Fuel tax bonds are typically required for fuel distributors, suppliers, wholesalers, importers, exporters, blenders, terminal operators, aviation fuel dealers, compressed natural gas dealers, liquefied natural gas dealers, and sometimes retail sellers. Specific requirements vary by state based on business activities, fuel types handled, and licensing classifications. Multi-state operators need separate bonds for each state where they conduct business.

How much does a fuel tax bond cost?

Fuel tax bonds typically cost between one percent and fifteen percent of required bond amounts annually. Applicants with excellent credit above 700 pay one to three percent, while those with poor credit below 600 pay seven to fifteen percent. For a twenty-five thousand dollar bond, costs range from two hundred fifty dollars for excellent credit to three thousand seven hundred fifty dollars for poor credit. Bonds exceeding fifty thousand dollars require business financial statements for underwriting.

What states require fuel tax bonds?

Most states require fuel tax bonds with notable exceptions including Maine, Iowa, South Dakota, Maryland, and Alaska according to some sources. Texas, Illinois, Georgia, Oregon, Colorado, Virginia, and most other states mandate bonds for various fuel business types. Federal operations require separate taxable fuel bonds filed with the Internal Revenue Service on Form 928.

How are fuel tax bond amounts determined?

States use different calculation methods for determining required bond amounts. Texas requires bonds equal to twice the maximum tax that could accrue during a reporting period. Illinois sets minimum one thousand dollar bonds adjusted by the Department of Revenue. Georgia bases amounts on estimated tax liabilities between two thousand and one hundred thousand dollars. Federal bonds cannot exceed expected tax liability for a representative six-month period.

Can I get a fuel tax bond with bad credit?

Yes, specialized surety programs approve fuel tax bonds for applicants with bad credit including those with scores below 600, bankruptcies, tax liens, or collections. These high-risk programs charge higher premiums typically seven to fifteen percent of bond amounts and may require collateral or personal guarantees for very poor credit. Even high-risk applicants can obtain required bonds to maintain business operations.

What is an IFTA bond?

An International Fuel Tax Agreement bond guarantees that interstate motor carriers will pay fuel taxes owed to all participating jurisdictions. IFTA simplifies tax reporting by allowing carriers to file through one base jurisdiction instead of every state traveled. IFTA bonds protect revenue collection across all member jurisdictions including lower forty-eight states and ten Canadian provinces.

How long does it take to get a fuel tax bond?

Qualified applicants with good credit receive instant approval and same-day bond issuance for fuel tax bonds under fifty thousand dollars. Poor credit or bonds requiring manual underwriting take three to seven business days. Federal taxable fuel bonds filed with the IRS may require additional processing time for registration approval.

What happens if someone files a claim against my bond?

When state agencies file claims against fuel tax bonds, surety companies investigate to determine validity. Valid claims result in the surety paying the state up to the bond amount. You must then reimburse the surety for the entire claim payment plus investigation costs. Failure to repay results in bond cancellation, license suspension, and collection lawsuits. Most fuel tax claims involve unpaid taxes easily verified through state records.

Do I need separate bonds for each state?

Yes, fuel businesses must obtain separate bonds for each state where they operate. Bond coverage does not transfer across state lines. Multi-state operators need individual bonds meeting each state’s specific requirements, amounts, and filing procedures. Federal taxable fuel bonds filed with the IRS operate independently from state bonds.

Conclusion

Fuel tax bonds protect state revenue collection while enabling legitimate fuel businesses to operate legally across the United States. These surety bonds transfer the financial burden of tax enforcement from government agencies to private insurance markets, creating a self-regulating system that screens out high-risk operators while providing financial recourse for unpaid taxes.

Understanding bond requirements by state, cost factors, claims processes, and licensing procedures helps fuel businesses maintain proper compliance and avoid costly violations. Most states require bonds ranging from one thousand to six hundred thousand dollars, with premiums typically between one and fifteen percent based on credit profiles.

Maintaining continuous bond coverage, understanding the three-party structure, navigating state-specific regulations, and staying current on tax obligations keeps fuel businesses compliant and competitive. The bonding process typically takes one to seven days for qualified applicants, making it straightforward to meet licensing requirements and start distributing fuel legally.

Five Facts About Fuel Tax Bonds

The International Fuel Tax Agreement emerged in 1983 when Arizona, Iowa, and Kansas created a fuel tax reciprocity program to simplify interstate trucking taxation. IFTA expanded to include all lower forty-eight states and ten Canadian provinces by 1996, fundamentally changing how motor carriers report and pay fuel taxes. Before IFTA, interstate carriers obtained licenses and filed quarterly returns in every jurisdiction traveled, creating overwhelming administrative burdens and compliance costs.

Federal taxable fuel bonds filed with the IRS on Form 928 operate under continuous liability with no fixed expiration dates or renewal terms. Unlike state bonds that renew annually, federal bonds remain perpetually active until formally canceled by the surety company or released by the Internal Revenue Service. This continuous structure means businesses can face unlimited liability for tax obligations spanning multiple years unless they properly terminate bonds when ceasing operations.

Texas fuel tax bond calculation formulas requiring twice the maximum tax per reporting period create the highest bond amounts in the nation. Large fuel distributors handling millions of gallons monthly can face six hundred thousand dollar bond requirements, generating annual premiums between six thousand and ninety thousand dollars depending on credit. These extreme bonding costs create significant barriers to entry in the Texas fuel distribution market.

Dyed diesel fuel bonds carry lower minimum amounts than regular diesel because dyed fuel receives tax exemptions for off-road agricultural and industrial uses. The red dye marker identifies tax-exempt fuel, and using dyed diesel in highway vehicles constitutes serious tax evasion. Enforcement agencies conduct random roadside inspections checking fuel tank contents for illegal dye use, and violations trigger massive penalties plus bond claims for unpaid road taxes.

Some states allow fuel businesses to post cash deposits or certificates of deposit instead of surety bonds, though fewer than ten percent of businesses use these alternatives. A twenty-five thousand dollar cash deposit ties up capital that could otherwise fund inventory purchases, facility improvements, or business expansion. The annual premium for a twenty-five thousand dollar bond averaging five hundred dollars saves twenty-four thousand five hundred dollars compared to cash deposit requirements.

Leave a Reply