You have heard the term “surety bond” thrown around in construction, courtrooms, and business contracts. But what does it actually mean? And why does every government contract seem to require one? This guide provides the complete legal and practical definition of a surety bond, based on the top ten authoritative sources, so you understand exactly what you are getting into before you sign.

The Simple Definition

A surety bond is a three-party agreement that guarantees one party (the principal) will fulfill their obligations to another party (the obligee). If the principal fails to perform, the third party (the surety) pays the obligee and then seeks repayment from the principal .

Think of it as a performance guarantee backed by a financial institution. Unlike insurance, which protects the policyholder, a surety bond protects the person or organization hiring the principal .

The Three Parties in Every Surety Bond

Every surety bond involves exactly three parties, each with distinct roles and responsibilities .

| Party | Role | Real-World Example |

|---|---|---|

| Principal | The party who needs the bond and must perform the obligation | A contractor bidding on a government project |

| Obligee | The party who requires the bond and benefits from the protection | The government agency awarding the contract |

| Surety | The company that guarantees the principal’s performance and backs the bond | An insurance company licensed to issue surety bonds |

The surety bond is the written instrument that “bonds” the surety to this obligation . Without a surety willing to back the principal, there is no bond.

The Legal Definition

Multiple authoritative legal sources define a surety bond consistently.

Cornell Law School’s Legal Information Institute (LII) defines a surety bond as “a three-party bond agreement involving the principal (the one who needs the bond), the obligee (the one who requires it), and the surety (the one who guarantees the principal’s performance). It acts like a security deposit, ensuring that legal or contractual duties are fulfilled” .

Indiana Administrative Code provides a statutory definition: “Surety bond means a contractual arrangement between the surety, the principal, and the obligee that the surety agrees to protect the obligee if the principal defaults in performing the principal’s contractual obligation” .

The American Heritage Dictionary offers a concise definition: “A guarantee issued by a surety agency on behalf of a client, requiring the agency to pay a sum of money to a third party in the event the client fails to fulfill certain obligations” .

What a Surety Bond Does

A surety bond serves three essential functions :

- Guarantees performance: It assures the obligee that the principal will complete the contracted work or fulfill their legal duty

- Provides financial protection: If the principal defaults, the surety pays the obligee up to the bond’s penal sum

- Creates accountability: The principal must reimburse the surety for any claim paid, creating strong incentive to perform

The guaranteed amount is called the penal sum—the maximum amount the surety will pay if the principal defaults .

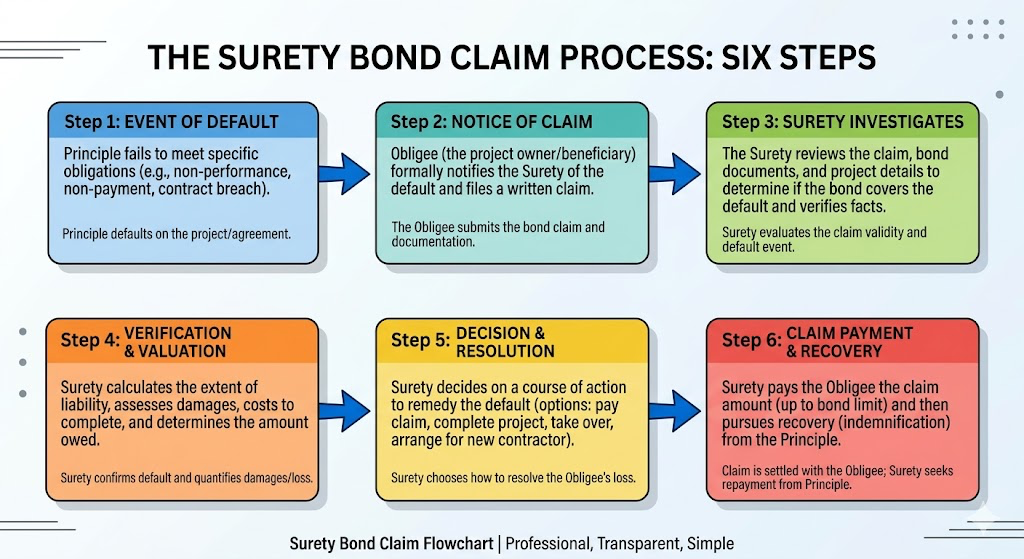

How a Surety Bond Works in Practice

Here is a step-by-step example of how a surety bond functions in a real-world scenario :

Step 1: The Contract

A general contractor (obligee) hires a subcontractor (principal) to install windows on a new hospital. The project owner wants a financial guarantee that the subcontractor will perform on time.

Step 2: The Bond

The subcontractor purchases a surety bond from a surety company. The bond guarantees the subcontractor’s performance according to the contract.

Step 3: The Default

The subcontractor fails to install the windows as agreed, causing delays and financial losses.

Step 4: The Claim

The general contractor files a claim against the bond. The surety investigates.

Step 5: The Payment

If the claim is valid, the surety pays the general contractor for the financial costs of non-performance—enough to hire another window company to complete the work.

Step 6: The Reimbursement

The surety then seeks full reimbursement from the subcontractor, plus any legal fees and costs incurred.

Surety Bond vs. Insurance: The Critical Difference

Many people confuse surety bonds with insurance policies because both are often sold by insurance companies. But they are fundamentally different .

| Feature | Surety Bond | Insurance |

|---|---|---|

| Number of parties | 3 parties (Principal, Obligee, Surety) | 2 parties (Insured, Insurer) |

| Who is protected | The obligee (client, government, or public) | The insured policyholder |

| Who ultimately pays claims | The principal (must reimburse the surety) | The insurer (no repayment required) |

| Loss expectation | Loss is not expected; underwriting prevents bad risks | Loss is factored into pricing |

| Underwriting focus | Credit, financial strength, and character | Actuarial risk pools and claims history |

Key takeaway: If an insurance company pays a claim, you do not pay them back. If a surety pays a claim, you owe them every dollar .

Surety Bond vs. Fidelity Bond

A fidelity bond is another common point of confusion. Despite the name “bond,” a fidelity bond is actually a form of insurance .

Surety Bond: A three-party guarantee that protects the obligee (client or government) if the principal fails to perform contractual obligations .

Fidelity Bond: A two-party insurance policy that protects an employer from losses caused by the dishonest acts of its employees. It covers losses of company monies, securities, and other property from employees who have a manifest intent to cause the company loss .

While called bonds, fidelity obligations are really insurance policies. They protect the employer, not a third party .

Surety Bond vs. Guarantee

A surety bond is similar to but distinct from a guarantee .

Surety Bond: A three-party agreement where the surety guarantees the principal’s obligations to the obligee. All three parties are directly involved.

Guarantee: A two-party agreement where one party (the guarantor) promises to cover the debt of another party (the debtor) to a third party (the creditor).

In practice, the terms are often used interchangeably, but the three-party structure of a surety bond is a key legal distinction .

Common Types of Surety Bonds

Surety bonds are used across many industries and situations. The most common types include :

Where Surety Bonds Are Required

Surety bonds are common in specific industries and situations .

Construction Industry: This is the largest market for surety bonds. Contractors need bid, performance, and payment bonds for public works projects and many private developments . The Miller Act requires surety bonds on most federal construction contracts .

Fiduciary Roles: Many jurisdictions require guardians, trustees, executors, and administrators to post a surety bond before taking responsibility for managing another person’s assets .

International Transactions: A company making a large purchase from a foreign supplier might require the supplier to post a surety bond to guarantee delivery .

Licensing: States require license bonds for many professions, including contractors, auto dealers, mortgage brokers, and freight forwarders .

Legal Proceedings: Courts require appeal bonds, supersedeas bonds, and other judicial bonds to protect parties during litigation .

How to Get a Surety Bond

The process follows four simple steps, and specialists like Swiftbonds have placed these bonds for businesses nationwide, working with A.M. Best A-rated sureties. Here is how it works:

- Apply: Complete a surety bond application with your business information, credit details, and the specific bond requirements.

- Quote: Within hours, the surety returns a premium quote based on your credit profile and financial strength.

- Pay: You pay the premium via credit card, ACH, or wire transfer.

- File: The surety issues the bond, and you file it with the obligee as required.

Swiftbonds LLC

2024 Surety Bond Provider of the Year

4901 W. 136th Street

Leawood KS 66224

(913) 214-8344

https://swiftbonds.com/

Frequently Asked Questions

Q: Is a surety bond a type of insurance?

No. While surety bonds are often issued by insurance companies, they are fundamentally different products. A surety bond is a three-party guarantee of performance, while insurance is a two-party risk transfer agreement .

Q: Who pays for a surety bond?

The principal pays the premium. This is typically the contractor or business that needs the bond .

Q: What happens if a claim is filed against my bond?

The surety investigates the claim. If valid, the surety pays the obligee up to the bond amount. You then must reimburse the surety in full, plus legal fees and costs .

Q: How is the bond amount determined?

The bond amount (penal sum) is set by the obligee or by statute. For performance bonds, it is typically 100% of the contract value. For license bonds, it is a fixed amount set by state law.

Q: Can I get a surety bond with bad credit?

Yes, but you will pay a higher premium. Some sureties have programs for applicants with challenged credit. However, sureties are more selective than insurers because they expect you to repay any claims .

Q: What is the difference between a surety bond and a fidelity bond?

A surety bond is a three-party guarantee protecting the obligee. A fidelity bond is a two-party insurance policy protecting an employer from employee theft, despite the confusing name .

5 Interesting Things About Surety Bonds Not in the Top 10 Sites

- Surety bonds predate insurance by centuries. The earliest surety-like agreements appear in the Code of Hammurabi (circa 1754 BC), where builders were held responsible for structural failures. The first corporate surety in the United States was the New York Guarantee and Indemnity Company, founded in 1837—decades before modern insurance markets matured.

- The surety can force the claimant to sue the principal first. Under some state laws, a surety can insist that the claimant bring an action against the principal and pursue it to judgment and collection before the surety is required to pay. This is called the “exhaustion of remedies” requirement and is a powerful protection for sureties.

- The indemnity agreement you sign pierces the corporate veil. When you purchase a surety bond, you typically sign a general indemnity agreement that makes you personally liable for any claim—even if your business is an LLC or corporation. This contractual waiver of limited liability is unique to surety bonds.

- Surety bonds are used in criminal cases too. In some jurisdictions, a surety bond can be executed to ensure the presence of an accused person in court. Such a bond is executed for the purpose of ensuring the accused appears at trial, allowing them to remain free during the proceedings .

- The surety market is highly concentrated. The top 10 surety companies in the United States write the vast majority of all contract bonds. This concentration means that contractors with poor credit or limited financials may find few options, as smaller sureties are often unwilling to take on higher-risk principals.

Conclusion

A surety bond is a three-party agreement in which the surety guarantees the principal’s performance to the obligee. If the principal defaults, the surety pays the obligee and then seeks reimbursement from the principal. This definition is consistent across legal sources, from the Cornell Legal Information Institute to state administrative codes to the American Heritage Dictionary .

Unlike insurance, which protects the policyholder and does not require repayment, a surety bond protects the obligee and holds the principal ultimately responsible for any claim paid . This fundamental difference shapes everything about how surety bonds are underwritten, priced, and enforced.

Surety bonds are required in construction, fiduciary relationships, international transactions, licensing, and legal proceedings . The most common types include bid bonds, performance bonds, payment bonds, license bonds, court bonds, and subdivision bonds .

Before signing any surety bond agreement, understand that you are personally guaranteeing your performance. The bond is not a safety net—it is a promise backed by your financial future.

Leave a Reply