You are a plan sponsor. You have employees. You offer a 401(k). But did you know that if you do not have a fidelity bond, you could be personally liable for any losses caused by fraud or theft? This is not optional. The Employee Retirement Income Security Act of 1974 (ERISA) is clear: every person who handles plan funds must be bonded. This guide covers everything you need to know about ERISA bonds—who needs them, how much coverage is required, what they cost, and how to avoid costly compliance mistakes.

What Is an ERISA Bond?

An ERISA bond (also called an ERISA fidelity bond) is a type of fidelity bond required by federal law that protects employee benefit plans—like 401(k)s and pension plans—against losses caused by acts of fraud or dishonesty by persons who handle plan funds .

The bond is not insurance for the plan sponsor. It is a protection for the plan itself and its participants. If someone with access to plan assets commits theft, embezzlement, or other dishonest acts, the bond covers the loss up to the bond amount .

ERISA was enacted in 1974 to address “public concern that private pensions and other employee benefit plans were being mismanaged and abused,” according to the U.S. Department of Labor . The bonding requirement—found in ERISA Section 412 (29 U.S.C. § 1112)—is a core part of that protection .

Who Needs an ERISA Bond?

Anyone who “handles funds or other property” of an employee benefit plan must be bonded . The Department of Labor defines “handling” functionally—it covers duties or activities that could cause a loss due to fraud or dishonesty, including acting alone or in collusion .

Who is typically covered:

- Plan administrators and trustees

- Anyone with check-signing authority

- Payroll staff who handle plan contributions

- Investment managers and advisers

- Third-party administrators (TPAs) with access to plan funds

- Anyone who exercises custody or control over plan assets

The bond must be written for the plan’s benefit—the plan is typically the named insured, not the individual fiduciary .

Exemptions (Who Does NOT Need an ERISA Bond)

How Much ERISA Bond Coverage Do You Need?

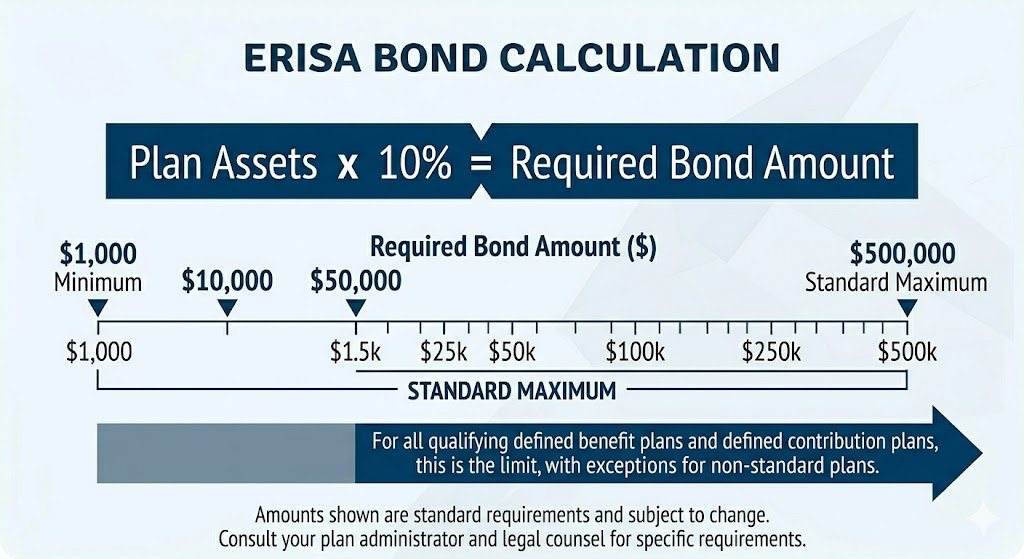

The required bond amount is 10% of the amount of plan funds handled in the preceding year .

| Requirement | Amount |

|---|---|

| Minimum bond | $1,000 |

| Standard maximum (most plans) | $500,000 |

| Higher maximum (plans with employer securities) | $1,000,000 |

Example calculation: If your plan has $2,000,000 in assets, you need a bond of at least $200,000 (10% of $2,000,000). If your plan has $10,000,000 in assets, the 10% calculation would suggest $1,000,000, but the cap applies: most plans cap at $500,000. Plans that hold employer securities can go up to $1,000,000 .

Important: If your plan assets increase, your bond amount must increase accordingly. Many plans fall out of compliance simply because the bond was not updated as assets grew .

What an ERISA Bond Covers (and Does NOT Cover)

What the Bond Covers

An ERISA fidelity bond protects the plan against losses caused by fraud or dishonesty by persons who handle plan assets . This includes:

- Theft and embezzlement

- Misappropriation of plan funds

- Fraudulent acts by plan fiduciaries

- Dishonest acts by third-party administrators

The bond is a “crime-protection device”—it is designed to respond when a dishonest taking occurs .

What the Bond Does NOT Cover

Critical distinction: The Department of Labor has drawn a clear line between bonding and fiduciary liability coverage. The ERISA fidelity bond insures against losses due to fraud or dishonesty. Fiduciary liability insurance generally addresses losses arising from alleged breaches of fiduciary responsibilities .

ERISA Bond vs. Fiduciary Liability Insurance vs. Crime Insurance

This is the most common point of confusion among plan sponsors .

| Coverage Type | What It Covers | Who It Protects | Required? |

|---|---|---|---|

| ERISA Fidelity Bond | Fraud, theft, dishonesty by persons handling plan funds | The plan and participants | Yes, by ERISA |

| Fiduciary Liability Insurance | Breach of fiduciary duty claims (e.g., poor investment choices, imprudent decisions) | The fiduciaries (individuals) | No, but recommended |

| Crime Insurance (Fidelity Bond) | Employee theft and dishonesty | The employer | No (but may be purchased) |

Key takeaway: These coverages are not interchangeable. Many plans mistakenly believe their fiduciary liability insurance satisfies the ERISA bond requirement. It does not .

How Much Does an ERISA Bond Cost?

ERISA bonds are surprisingly affordable. For coverage amounts up to $500,000, bonds are typically available at flat rates with no underwriting .

| Coverage Amount | Typical Premium Range |

|---|---|

| $10,000 – $500,000 | $100 – $452 (flat rate) |

| Above $500,000 | Subject to underwriting (varies) |

Premium rates generally range from $100 to $452 for coverage amounts between $10,000 and $500,000 . Some providers offer bonds with a 100% approval rate .

How to Get an ERISA Bond

The process follows four simple steps, and specialists like Swiftbonds can help plan sponsors obtain ERISA bonds quickly, working with Treasury-listed surety companies. Here is how it works:

- Apply: Complete a bond application with your plan information, including total plan assets and the plan’s legal name.

- Quote: Within minutes, the surety returns a premium quote based on your required bond amount (10% of plan assets).

- Pay: You pay the premium via credit card, ACH, or wire transfer—typically $100 to $452 for most plans.

- File: The surety issues the bond. You must keep it on file for plan records; there is no filing requirement with the DOL, but you must attest to coverage on Form 5500.

Swiftbonds LLC

2025 Surety Bond Agency of the Year

4901 W. 136th Street

Leawood KS 66224

(913) 214-8344

https://swiftbonds.com/

ERISA Bond Requirements for the Bond Itself

The bond must meet specific requirements to be compliant:

- Issuer must be qualified: The bond must be obtained from an insurer listed on the U.S. Department of the Treasury’s list of approved sureties (Circular 570)

- No deductible: ERISA requires first-dollar coverage—deductibles are not permitted

- Plan as named insured: The bond must be written for the plan’s benefit

- Covers all plan assets: The bond must apply to all plan assets regardless of asset type or custody arrangements

Common Compliance Mistakes to Avoid

1. Confusing ERISA Bond with Fiduciary Liability Insurance

This is the most common misunderstanding. Fiduciary liability insurance covers breaches of fiduciary duty. An ERISA bond covers theft and dishonesty. They are not interchangeable .

2. Assuming Small Plans Are Exempt

Audit exemptions do not apply to fidelity bonds. ERISA requires fidelity coverage regardless of plan size or number of participants .

3. Not Updating the Bond When Assets Grow

If your plan assets increase, your bond amount must increase to maintain 10% coverage. Many plans fall out of compliance simply because the bond was not updated .

4. Using a Bond with a Deductible

ERISA requires first-dollar coverage. Any policy with a deductible does not satisfy the bonding requirement .

5. Thinking Retroactive Coverage Can Fix Past Gaps

Insurers generally cannot issue retroactive bonds due to legal constraints. If you are discovered without coverage during a plan audit, you must work directly with the DOL to document remediation efforts .

Penalties for Non-Compliance

ERISA is clear that it is unlawful for non-exempt plans to not be bonded. Moreover, you could be held personally liable for any losses that a fidelity bond would otherwise cover .

Form 5500, filed annually under penalty of perjury, asks directly about fidelity bond coverage. Accurate compliance is essential .

5 Interesting Things About ERISA Bonds Not in the Top 10 Sites

- ERISA bonds are technically not “insurance” under state law. Unlike traditional insurance policies that are regulated by states, ERISA bonds are governed by federal law and must be issued by sureties on the U.S. Treasury’s approved list—a distinction that matters for claims handling and regulatory oversight.

- The $1,000 minimum applies even to very small plans. If your plan has only $5,000 in assets, 10% would be $500—but the statutory minimum is $1,000, so you still need a $1,000 bond .

- H.R. 2988 (2025-2026) does NOT change ERISA bond requirements. Despite significant fiduciary reform proposals in Congress, none of them amend ERISA Section 412, which governs the fidelity bond requirement. The bonding requirement remains unchanged .

- Third-party administrators may need separate coverage. If your TPA “handles” plan funds—meaning they have check-signing authority or custody of assets—they must be covered by an ERISA bond, either under your bond or their own .

- The bond protects against collusion, not just individual acts. The DOL explicitly states that the bond covers dishonest acts “acting alone or in collusion with others,” meaning coordinated theft by multiple employees is still covered .

Conclusion

An ERISA bond is a federally required fidelity bond that protects employee benefit plans from losses caused by fraud or dishonesty by persons who handle plan funds. Anyone who “handles” plan assets must be bonded. The required bond amount is 10% of plan assets handled in the preceding year, with a minimum of $1,000 and a standard maximum of $500,000 ($1,000,000 for plans holding employer securities).

The bond must be issued by a Treasury-listed surety, must have no deductible, and must name the plan as the insured. It is not interchangeable with fiduciary liability insurance or crime insurance. Common compliance mistakes include confusing these coverages, failing to update bonds as assets grow, and assuming small plans are exempt.

Before your next compliance review, verify that your ERISA bond amount is adequate (10% of current plan assets), that it is issued by an approved surety, and that all persons who handle plan funds are covered. The bond is not optional—it is a condition of lawful plan operation.