You want a surety bond. But before the surety company says yes, they need to know one thing: can you pay them back if something goes wrong? Unlike insurance, where claims are expected and pooled across many policyholders, surety bonds are underwritten to a 0% loss ratio. The surety assumes you will not default. To make that bet, they need to qualify you—and the process is rigorous. This guide explains exactly what sureties look for, the qualifications you need, and how to get approved.

The Core Principle: Surety Bonds Are Credit, Not Insurance

The most important thing to understand is that a surety bond is not insurance. Insurance protects the policyholder. A surety bond protects the obligee—the person or agency requiring the bond. And if the surety pays a claim, the principal (you) must reimburse the surety in full .

This fundamental difference means sureties underwrite bonds like a bank underwrites a loan. They are evaluating your ability to repay them if they have to pay out on your behalf. Your premium is not a pooled risk payment—it is a service fee for the use of the surety’s financial backing .

The Three Parties to Every Surety Bond

Every surety bond involves exactly three parties :

| Party | Role | Who They Are |

|---|---|---|

| Principal | The person or business who needs the bond and must perform the obligation | You—the contractor, auto dealer, notary, or business owner |

| Obligee | The party requiring the bond and benefiting from the protection | Government agency, licensing board, or project owner |

| Surety | The company that issues the bond and backs the guarantee | A.M. Best A-rated insurance company authorized to write surety bonds |

If the principal fails to meet their obligations, the obligee can file a claim against the bond. The surety investigates and, if the claim is valid, pays the obligee up to the bond amount. The principal must then reimburse the surety .

Primary Qualification Factors for a Surety Bond

Sureties evaluate applicants using several key criteria. Your credit score is the most important factor, but not the only one.

1. Personal Credit Score (Most Important Factor)

Your personal credit score is the single biggest factor affecting both your eligibility and your premium rate . Sureties use credit to predict your likelihood of repaying them if they pay a claim.

| Credit Category | Score Range | Typical Premium Rate |

|---|---|---|

| Excellent | 675 and above | 0.5% – 3% of bond amount |

| Good | 650 – 674 | 1% – 5% |

| Average | 600 – 649 | 4% – 10% |

| Poor | 599 and below | 10% – 15%+ |

What sureties look for on your credit report:

- Payment history on past debts

- Outstanding balances and credit utilization

- Length of credit history

- Recent credit inquiries

- Bankruptcies, judgments, or liens

A credit score of 650 or higher is generally considered good for bonding purposes . Applicants with scores below 600 can still get bonded, but premiums will be significantly higher.

2. Years in Business and Industry Experience

Sureties prefer to bond businesses with a proven track record. The longer you have been in business, the lower the risk .

| Years in Business | Qualification Impact |

|---|---|

| 5+ years | Strongest qualification; lowest rates |

| 2-4 years | Standard qualification; moderate rates |

| Less than 2 years | May require additional documentation or higher rates |

| Start-up / No history | May need SBA guarantee or collateral |

What sureties look for:

- Business longevity and stability

- Industry-specific experience

- Past project completion history

- Previous bonding history (if any)

3. Business Financial Strength

For larger bonds, sureties review your business financials to assess your capacity to repay claims .

| Financial Metric | What Sureties Look For |

|---|---|

| Working capital | Positive, with strong liquidity |

| Net worth | Growing year over year |

| Profitability | Consistent net profit on projects |

| Debt-to-equity ratio | Low leverage |

| Cash flow | Sufficient to cover operations and potential claims |

Required documentation for larger bonds:

- 2-3 years of business tax returns

- Balance sheet

- Income statement (profit and loss)

- Cash flow statement

- Accounts receivable aging report

4. Bond Type and Amount

Different bond types have different qualification requirements. License and permit bonds are generally easier to qualify for than large performance bonds .

Surety Company Qualifications: The Other Side of the Equation

When a contract requires a bond, the surety company itself must be qualified. Government contracts, in particular, have strict requirements for which sureties are acceptable .

Treasury Department Circular 570

The U.S. Department of the Treasury maintains a list of surety companies acceptable on federal bonds, known as Department Circular 570 . For any federal bond—or many state and local bonds—the surety must appear on this list.

Key requirements for sureties on federal bonds:

- Certificate of Authority from the Treasury Department

- Minimum underwriting limitations based on financial strength

- Compliance with 31 CFR Part 223

A.M. Best Rating Requirements

Many government contracts require the surety to have a minimum A.M. Best rating .

| Bond Amount | Minimum A.M. Best Rating | Minimum Financial Size Category |

|---|---|---|

| Up to $1,000,000 | B+ | Class I |

| $1M – $2M | B+ | Class II |

| $2M – $5M | A | Class III |

| $5M – $10M | A | Class IV |

| $10M – $25M | A | Class V |

| $25M – $50M | A | Class VI |

| Over $50M | A | Class VII |

Florida Qualification Standards (Example)

A typical “Qualification of Surety” clause from a Florida municipality requires :

- Surety must be authorized to do business in Florida

- Surety must have a resident agent in Florida

- Surety must have been in business for at least five years

- Surety must hold a current Treasury Circular 570 Certificate

- For bonds over $500,000: A.M. Best rating of A- or better

- For bonds over $2M: A.M. Best rating of A or better

Special Qualification Programs

SBA Preferred Surety Bond (PSB) Program

The Small Business Administration helps small contractors obtain surety bonds through the PSB program . To qualify as a PSB surety, a company must have:

- Underwriting limitation of at least $6,500,000 on Treasury Circular 570

- Agreement not to charge excessive premiums

- Underwriting authority vested only in employees of the surety

- Acceptable rating from recognized authorities

For contractors: The SBA guarantee helps you get bonded even if you would not qualify on your own. The surety shares the risk with SBA.

License and Permit Bond Simplified Qualification

License and permit bonds are among the easiest bonds to qualify for . Many are issued with:

- No credit check (or only a soft credit pull)

- Flat rate premiums starting at $100

- Instant online issuance

This is because these bonds are considered lower risk—the bond amount is typically smaller, and claims are less frequent.

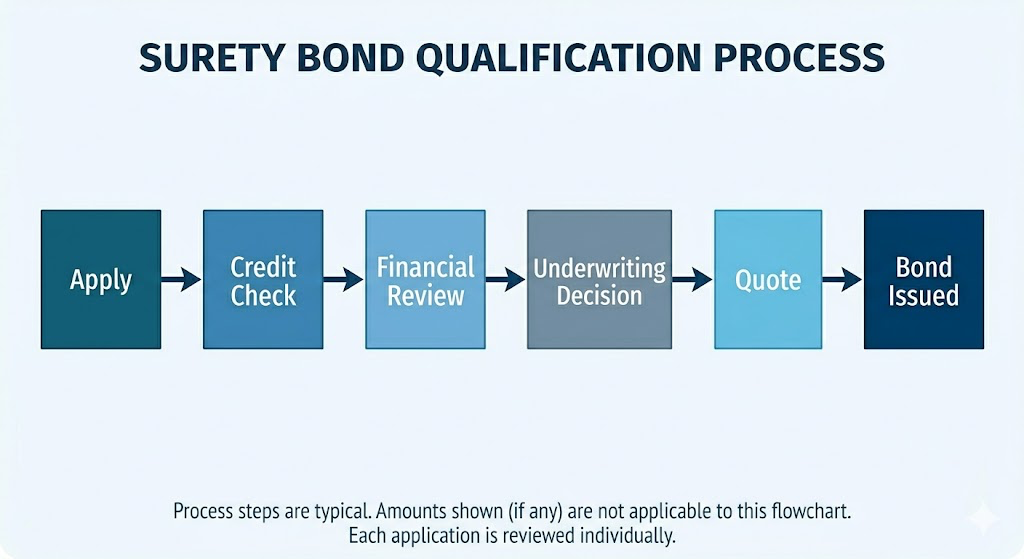

Step-by-Step: How to Get Qualified for a Surety Bond

The process follows these steps, and specialists like Swiftbonds have helped businesses get bonded nationwide since 2008, working with A.M. Best A-rated sureties. Here is how it works:

- Apply: Complete a surety bond application with your business information, personal credit details, and the specific bond type and amount required.

- Credit Check: The surety reviews your personal credit report. For smaller bonds, this may be a soft pull that does not affect your credit score.

- Underwriting Review: For larger bonds, the surety reviews your business financials, years in operation, and industry experience .

- Quote: Within hours (or minutes for small bonds), the surety returns a premium quote based on your qualifications.

- Pay and File: You pay the premium, the surety issues the bond, and you file it with the obligee.

Swiftbonds LLC

Voted 2025 Surety Bond Agency of the Year

4901 W. 136th Street

Leawood KS 66224

(913) 214-8344

https://swiftbonds.com/

What Disqualifies You from Getting a Surety Bond?

While few applicants are completely disqualified, certain factors make approval difficult or expensive:

| Factor | Impact on Qualification |

|---|---|

| Recent bankruptcy (within 3 years) | High risk; may require collateral or SBA guarantee |

| Outstanding bond claims | Very high risk; many sureties will decline |

| Poor credit (below 550) | High premiums (15%+); may require cash deposit |

| No business history or experience | May be declined for larger bonds |

| Active tax liens or judgments | Negative impact; must be disclosed |

If you are disqualified: Some states allow cash deposits in lieu of surety bonds. You deposit the full bond amount with the state treasurer, and they hold it as security. However, this ties up your working capital, while a surety bond only requires a small premium payment.

Frequently Asked Questions

Q: Do I need good credit to get a surety bond?

Yes, credit is the most important factor. However, applicants with poor credit can still get bonded—premiums will be higher (10-15% instead of 1-3%). Some sureties specialize in challenged credit .

Q: What is the minimum credit score for a surety bond?

There is no official minimum, but scores below 550 make approval difficult and expensive. A score of 650 or higher is considered good .

Q: How long does it take to get qualified?

For small license and permit bonds, approval can be instant or within hours. For larger performance bonds, underwriting may take several days .

Q: Do I need financial statements for a surety bond?

For smaller bonds (under $25,000), typically no. For larger bonds, sureties usually require 2-3 years of business financial statements .

Q: Can a start-up business get a surety bond?

Yes, but you may pay higher premiums. For larger bonds, you may need an SBA guarantee or collateral .

Q: What is the difference between being bonded and being insured?

Insurance protects you. A bond protects your customers or the government. If a claim is paid on your bond, you must repay the surety .

Q: Can a surety bond be cancelled?

Yes. Most continuous bonds require the surety to provide notice—typically 30 to 60 days—before cancellation .

5 Interesting Things About Surety Bond Qualifications Not in the Top 10 Sites

- Bid bonds are often free and require no qualification. Many sureties issue bid bonds at no cost because they expect to write the performance bond if you win. This means you can bid on projects without any upfront bonding cost or qualification process .

- The SBA PSB program has a “work commencement” rule. Under 13 CFR 115.64, if work begins before the bond is approved, the surety loses SBA guarantee protection—unless they obtain prior written approval from SBA .

- Sureties can be rejected by the obligee even if you qualify. Under many “Qualification of Surety” clauses, the project owner can reject a surety company if they do not meet minimum rating requirements—forcing the contractor to find a new surety without increasing the bid .

- Florida requires sureties to have a resident agent. This is unusual—most states do not require surety companies to maintain a physical agent within state lines. Florida’s requirement is explicitly stated in many municipal bond clauses .

- The Treasury Circular 570 list is updated quarterly. The list of acceptable sureties on federal bonds is not static—companies can be added or removed. Contractors should verify their surety is still on the list before submitting a bid .

Conclusion

Getting qualified for a surety bond requires understanding that sureties underwrite bonds like credit, not like insurance. Your personal credit score is the most important factor, followed by your years in business and financial strength . For smaller license and permit bonds, qualification is simple—often with no credit check and instant approval. For larger performance bonds, full underwriting is required.

Sureties themselves must also be qualified. For government contracts, the surety must appear on the U.S. Treasury Department’s Circular 570 and may need minimum A.M. Best ratings based on the bond amount . The SBA’s Preferred Surety Bond program helps small contractors obtain bonds they might not qualify for on their own .

Before applying for any surety bond, check your credit score, gather your business financials (for larger bonds), and work with an experienced surety agent who can find the best rate for your specific qualifications.